Quick reference — retirement contribution limits (2025 & 2026)

Retirement contribution limits — 2025 and 2026:

| Plan | 2025 | 2026 |

|---|---|---|

| 401(k) elective deferral | $23,500 | $24,500 |

| 401(k) age-50 catch-up | +$7,500 | +$8,000 |

| 401(k) SECURE 2.0 age 60–63 catch-up | +$11,250 | +$11,250 |

| Traditional & Roth IRA | $7,000 (+$1,000 age 50+) | $7,500 (+$1,100 age 50+) |

| SIMPLE IRA (employee) | $16,500 (+$3,500 age 50+) | $17,000 (+$4,000 age 50+) |

Sources: IRS — 401(k) Contribution Limits · IRS — IRA Limits · IR-2024-285 (2025 announce). Verified May 2026.

It’s important for small business owners to have a plan for retirement.

If you own an S corporation, there are several options available to you. In today’s post, I’ll give you the lowdown on the five main options so you can think through what’s best for your company and your future.

Individual Retirement Account (IRA) and 401(k)

The two most common types of retirement accounts are IRAs and 401(k)s. As an S corporation owner, you can choose from both of those types, and I’ll discuss them both in this post.

The two types of IRAs used most commonly by S corporation owners are traditional IRAs and Roth IRAs. These two types of accounts have several things in common, so I’ll discuss those first and then I’ll let you know what distinguishes one from the other and how that applies to your taxes.

Both traditional and Roth IRAs can be opened by pretty much anyone with taxable income and the accounts can be opened through a bank, brokerage, or other financial institution. As an S corporation shareholder-employee, you can contribute your earned income to these accounts, but you cannot contribute any distributions you receive from the company.

In 2026, the total amount you can contribute to all of your traditional and Roth IRAs combined is up to $7,500 per year if you’re under age 50 (up from $7,000 in 2025). Those aged 50 and older can contribute an additional $1,100 per year, making the total $8,600 per year for all traditional and Roth IRAs combined.

One important note is that if you withdraw money from a retirement plan, no matter if it’s an IRA or 401(k) before you reach the age of 59 ½, that’s called an early distribution. Unless you’re withdrawing contributions from a Roth IRA, you will be charged an additional 10% tax. There are some very specific exceptions to this additional tax, but you shouldn’t count on withdrawing early if you can help it.

Oh, and one more fun thing to note (we use the term fun loosely around here) is that the deadline for making IRA contributions is typically not until the tax deadline of the following year. So if you wanted to reap the tax benefits of making retirement contributions on your 2025 taxes, you had until April 15, 2026 to do so. One caveat for 401(k)s: if you’re an S corporation owner on payroll, your employee 401(k) deferrals have to run through your paychecks by December 31 — only employer contributions can wait until the return due date.

Traditional IRA

Alright, let’s get into some differences between the two most common IRAs. The biggest difference between a traditional and Roth IRA is that with a traditional IRA, you won’t pay any taxes until you withdraw funds. This is a good strategy and retirement account to use if you think you will be in a lower tax bracket when you retire than you are now.

Contributing to a traditional IRA allows you to receive a tax benefit when you contribute since your yearly contribution is a deduction from your taxable income. However, if you or your spouse is covered by a retirement plan at work, then the deduction may be phased out (reduced) or eliminated. This will depend on your filing status and income.

Another key difference is that a traditional IRA has a required minimum distribution starting at age 73 (SECURE 2.0 raised this from 72, and it rises to 75 in 2033), which means that you must take a yearly taxable withdrawal from your account.

Roth IRA

The big difference with the Roth IRA is that rather than delaying paying your taxes until you withdraw money when you’re retired, you’ll actually pay your taxes up-front and contribute after-tax dollars to your Roth IRA. This can make the Roth IRA the better choice for those who expect to be in a higher tax bracket when they retire than they are now.

Another difference is that your Roth IRA contribution is limited (phased out or eliminated entirely) based upon your income and filing status. For instance, in 2026, the amount you can contribute starts phasing out if you file as:

- Single or head of household with modified adjusted gross income (MAGI) of more than $153,000 (for 2025, the phaseout started at $150,000)

- Married, filing jointly with a MAGI of more than $242,000 (for 2025, $236,000)

- Married, filing separately — your contribution starts phasing out with any MAGI above $0 and disappears entirely at $10,000

Unlike with a traditional IRA, when your money is in a Roth IRA, you can make tax-free and penalty-free withdrawals on your contributions (but not your earnings!), and there are no minimum distribution requirements no matter your age.

Simplified Employee Pension IRA (SEP-IRA)

Now that we’ve discussed the two most common IRAs, there’s another type of IRA that we should put on your radar. Rather than employees setting up their own IRAs, a SEP-IRA is instead set up by the employer. This type of plan can be established by a business of any size, self-employed included.

An SEP-IRA allows you, as an S corporation owner, to create a retirement account where you can contribute up to 25% of each employee’s pay (including yours!) to the account (up to a maximum amount set by the IRS). And when you are the owner and the employee, this can be an effective way to save for retirement while lowering the company’s taxable income.

For example, if you pay yourself a salary of $75,000, the company can contribute up to $18,750 (that’s 25%) to your SEP-IRA on top of that salary. One thing to know: the contribution doesn’t shrink the Social Security and Medicare (FICA) taxes on your paycheck — those are still due on the full $75,000 of wages. But per the IRS, the employer SEP contribution itself isn’t subject to income tax withholding or FICA, and it’s deductible on the business’ tax return, so that reduces the company’s federal tax bill as well.

Other benefits of setting up a SEP-IRA are that it’s easy to create, has low administrative costs, and allows for flexibility in how much the employer contributes. Also, employees are always 100% vested in the account, which means they always have ownership over their money.

One important thing to remember with this type of IRA is that the employer must contribute the same percentage of compensation for all eligible employees. Like with traditional IRAs, SEP-IRAs require minimum distributions starting at age 73.

An added bonus for this choice is that you can contribute to an SEP-IRA as an employer and also contribute to a traditional or Roth IRA as an employee.

Savings Incentive Match Plan for Employees (SIMPLE IRA)

Another IRA available to small businesses (less than 100 employees) is the SIMPLE IRA. With this plan, the employee makes pre-tax contributions up to a maximum amount set by the IRS. The employer can either choose to match that contribution for up to 3% of the employee’s wages or set a 2% nonelective contribution for each eligible employee.

As an S corporation owner, having a SIMPLE IRA allows you to make pre-tax contributions as an employee and also earn the tax deduction for the contribution as the employer.

Similar to creating a SEP-IRA, benefits of setting up a SIMPLE IRA are that it’s easy to create and has low administrative costs. Also, employees are always 100% vested in the account, which means they always have ownership over their money.

The early withdrawal penalties are heftier with SIMPLE IRAs, however, as early withdrawals (before age 59 ½) taken in the first two years of the account being opened carry an additional tax penalty of 25% but then are subject to the 10% additional tax thereafter. Like with traditional and SEP-IRAs, SIMPLE IRAs require minimum distributions starting at age 73.

One-Participant 401(k)

A one-participant 401(k) is just what you’d think it would be based on that title: a 401(k) plan for a business owner without employees (except for a spouse). It can also be referred to as a Solo 401(k), Solo-k or Uni-k.

The one-participant 401(k) is a traditional 401(k) with the same rules and requirements as any other. For S corporation owners, this means that you will make an employee contribution, and the employer (also you!) will make an employer contribution up to a maximum amount set by the IRS.

An advantage to having a one-participant 401(k) is that the plan can allow you to make post-tax designated Roth (Roth 401(k)) contributions — these aren’t the same as Roth IRA contributions, and since 2024 designated Roth 401(k) accounts have no required minimum distributions during your lifetime. You will, however, be required to make minimum distributions from the pre-tax portion of your one-participant 401(k) starting at age 73.

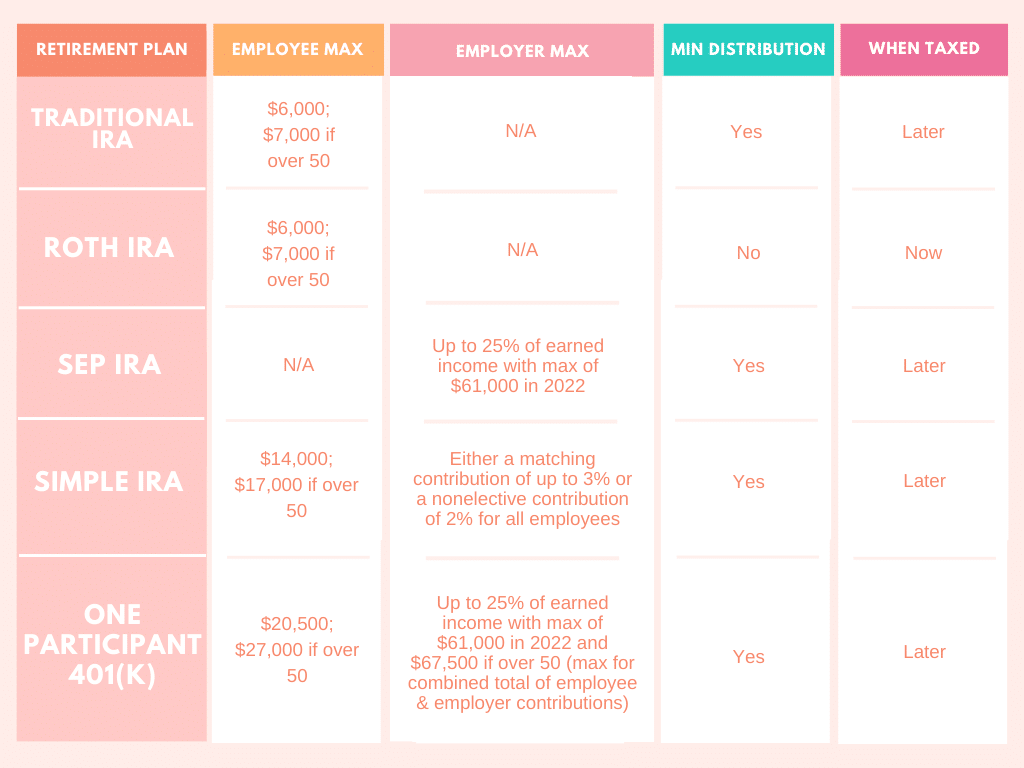

I thought I would wrap this up with a nice chart to help categorize the 5 types of retirement plans we discussed today. I hope you’ve found this information helpful and that it’s motivated you to start planning for your financial future.

If you have questions about retirement planning, make sure you contact a professional to help you sort it all out. And if you found this article helpful, take a minute to look through the other posts I’ve written for S corporation owners like you.